Knightscope (NASDAQ: KSCP) has positioned itself as a potential breakout player in the autonomous security robot market, with some analysts drawing comparisons to NVIDIA’s trajectory from gaming chip maker to AI infrastructure giant. The comparison hinges on a tangible partnership: Knightscope selected NVIDIA’s Jetson Xavier module to power its fifth-generation Autonomous Security Robots, embedding the same AI compute architecture that drives autonomous vehicles and industrial robotics into mobile security platforms. Whether KSCP can replicate NVIDIA’s 1,350% five-year surge remains speculative, but the company’s recent moves””including a Palantir partnership for federal market access and the unveiling of its K7 robot””suggest a deliberate strategy to become foundational infrastructure for physical security automation. The “Nvidia of Physical AI” framing is promotional language, not an official designation, and investors should approach it with appropriate skepticism.

However, the underlying thesis deserves examination. KSCP trades at approximately $3.72 per share with a market cap of roughly $42.8 million as of January 2026, a fraction of NVIDIA’s valuation. Analysts covering the stock have issued a “Strong Buy” rating with a consensus price target of $16.67, implying over 310% upside. This article examines the technical foundation, market positioning, financial realities, and strategic partnerships that inform both the bullish case and the substantial risks facing this small-cap security robotics company.

Table of Contents

- What Makes KSCP a Contender for the “Nvidia of Physical AI Security” Label?

- How Does the K7 Robot Represent Knightscope’s Technical Evolution?

- What Does the Palantir Partnership Mean for Federal Market Access?

- How Do Knightscope’s Financials Compare to Its Ambitions?

- What Are the Primary Risks to the KSCP Investment Thesis?

- How Does the NVIDIA Hardware Integration Create Technical Advantages?

- Where Does Physical AI Security Go From Here?

- Conclusion

What Makes KSCP a Contender for the “Nvidia of Physical AI Security” Label?

The comparison to NVIDIA stems from two factors: Knightscope’s use of NVIDIA hardware as core infrastructure and its ambition to become the default platform for autonomous security operations. CEO William Santana Li stated, “We are excited to leverage the massive investment NVIDIA has made in artificial intelligence for our future products,” when announcing the Jetson Xavier integration in 2021. The Jetson Xavier module provides edge AI computing capabilities””the same technology stack powering autonomous vehicles, warehouse robots, and industrial inspection systems””packaged for security applications. NVIDIA’s own trajectory offers a template. A decade ago, the company was primarily known for gaming graphics cards.

Today, it supplies the compute backbone for large language models, autonomous systems, and enterprise AI infrastructure. The bulls argue kscp could follow a similar path in physical security: starting with hardware deployments, accumulating proprietary data (the company claims over 3 million hours of AI training data), and eventually becoming indispensable infrastructure for security operations across commercial and government sectors. However, the comparison has limits. NVIDIA achieved dominance through network effects in software (CUDA) and developer ecosystems, not just hardware performance. Knightscope must demonstrate similar platform stickiness. Its Autonomous Security Robots are currently deployed at commercial properties, but the technology remains unproven at scale in high-security government installations where the margins and contract values would justify the NVIDIA comparison.

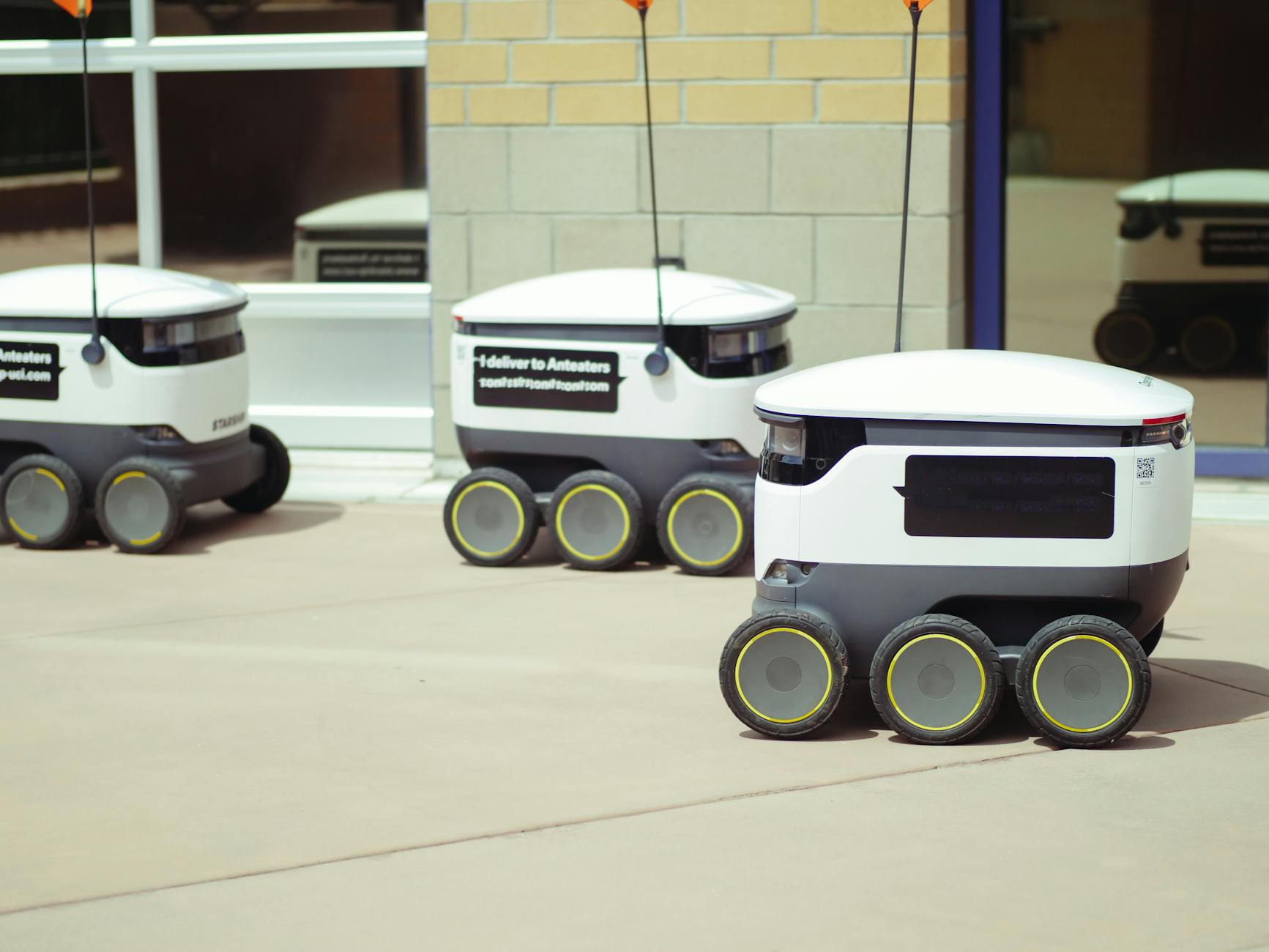

How Does the K7 Robot Represent Knightscope’s Technical Evolution?

Knightscope unveiled the K7 Autonomous Security Robot in November 2025, describing it as “the next evolution in Physical AI.” The robot targets large-area security applications: critical infrastructure, transportation hubs, logistics yards, industrial complexes, and defense installations. Unlike earlier models designed for indoor patrol and parking structures, the K7 addresses outdoor environments where human security patrols face limitations in coverage, consistency, and cost. Limited production deployment is expected in the second half of 2026, meaning the K7 remains pre-revenue for at least another six months. This timeline matters for investors evaluating near-term catalysts.

The company closed $12.1 million in financing to scale operations, but hardware manufacturing at scale introduces execution risk. Supply chain constraints, quality control issues, and deployment logistics have challenged robotics companies with more mature operations. The K7’s target markets””defense installations, critical infrastructure””also require security clearances and procurement processes that move slowly. Commercial deployments can happen in months; federal contracts often take years. Investors expecting rapid revenue growth from the K7 should calibrate expectations accordingly.

What Does the Palantir Partnership Mean for Federal Market Access?

In July 2025, Knightscope signed a two-year agreement with palantir Technologies under the FedStart program, providing a pathway to FedRAMP High and DoD Impact Level 5 accreditation. This partnership addresses one of the most significant barriers to federal security contracts: the compliance and infrastructure requirements that small companies cannot typically afford to build independently. Knightscope’s systems will operate within Palantir-managed AWS GovCloud clusters, giving federal agencies confidence that data from autonomous security robots meets government security standards. The partnership also provides sales channel access. Palantir has established relationships across defense, intelligence, and civilian agencies.

For a company with a $42.8 million market cap, piggybacking on Palantir’s federal presence represents a capital-efficient go-to-market strategy. The risk lies in dependency. Palantir controls the infrastructure and relationships. If the partnership sours or Palantir prioritizes competing solutions, Knightscope’s federal ambitions could stall. Additionally, FedRAMP and DoD accreditation processes take time””often 12 to 24 months””and require ongoing compliance investments. The partnership opens doors but does not guarantee contracts.

How Do Knightscope’s Financials Compare to Its Ambitions?

Q3 2025 revenue reached $3.1 million, up from $2.5 million in Q3 2024″”a 24% year-over-year increase. For a company positioning itself as transformative infrastructure, these numbers are modest. At current revenue run rates, Knightscope generates roughly $12 million annually against a market cap of $42.8 million, implying a price-to-sales ratio around 3.5x. That valuation is not extreme for a growth company, but it requires continued execution. The 52-week trading range tells a story of volatility: $2.45 to $12.47.

At current prices near $3.72, the stock sits closer to its lows than highs. The analyst consensus price target of $16.67 implies confidence in catalysts that have not yet materialized””K7 deployments, federal contracts, or strategic partnerships beyond Palantir. Analysts covering small-cap stocks often set optimistic targets, and coverage with only three analysts provides limited signal. The $12.1 million financing provides operational runway, but hardware companies burn capital faster than software businesses. Manufacturing, inventory, deployment logistics, and customer support all require upfront investment before recurring revenue materializes. Investors should monitor cash burn rates in upcoming quarterly reports.

What Are the Primary Risks to the KSCP Investment Thesis?

The most significant risk is execution. Robotics companies routinely underestimate the complexity of manufacturing at scale, deploying in diverse environments, and maintaining fleets of autonomous machines. Knightscope’s 3 million hours of AI training data provides a competitive moat in theory, but data alone does not prevent mechanical failures, software bugs in edge cases, or customer dissatisfaction with real-world performance. Competition presents another challenge. Boston Dynamics, with backing from Hyundai, has entered security applications.

Established security companies like ADT and Securitas are exploring automation. Startups in adjacent spaces””surveillance drones, fixed autonomous cameras with AI analytics””compete for the same security budgets. Knightscope’s advantage lies in ground-based mobile robots, but customers may ultimately prefer different form factors. Regulatory and liability questions remain unresolved. When an autonomous security robot misidentifies a threat or fails to detect an actual intrusion, liability allocation between the robot manufacturer, the security service provider, and the property owner remains legally untested at scale. High-profile failures could set back the entire category.

How Does the NVIDIA Hardware Integration Create Technical Advantages?

The Jetson Xavier module provides Knightscope’s robots with edge computing capabilities that enable real-time AI inference without constant cloud connectivity. This matters for security applications where network outages, latency, or bandwidth constraints could compromise operations. The robot can identify anomalies, recognize faces (where legally permitted), and detect environmental changes locally.

NVIDIA’s platform also provides a development ecosystem. Knightscope’s engineers can leverage NVIDIA’s software libraries, simulation tools, and continuous hardware improvements. As NVIDIA releases more powerful edge AI modules, Knightscope can upgrade its robots’ cognitive capabilities without redesigning core systems. This creates a technology partnership that extends beyond a single component purchase.

Where Does Physical AI Security Go From Here?

The broader physical AI security market is expanding as labor costs rise, security threats evolve, and autonomous technology matures. Knightscope is not the only company pursuing this opportunity, but its combination of deployed robots, accumulated training data, NVIDIA-powered computing, and federal market access through Palantir creates a differentiated position. The K7 deployment in the second half of 2026 will provide concrete evidence of whether the company can execute on its ambitions.

Whether KSCP becomes “the NVIDIA of Physical AI Security” depends on factors beyond any single product launch: sustained revenue growth, successful federal contract wins, competitive differentiation, and continued access to capital. The comparison to NVIDIA is aspirational marketing, but the underlying market opportunity for autonomous security infrastructure is real. Investors should evaluate the company on execution metrics, not analogies.

Conclusion

Knightscope occupies an interesting position in the emerging physical AI security market. Its NVIDIA-powered robots, Palantir partnership for federal access, and K7 platform for large-area security address genuine market needs. The analyst “Strong Buy” rating with a $16.67 price target reflects optimism about catalysts in the K7 deployment and federal market entry. However, the $42.8 million market cap and $3.1 million quarterly revenue indicate a company still proving its commercial viability.

The “Nvidia of Physical AI Security” framing is promotional, but the underlying question is valid: can a small robotics company become foundational infrastructure for autonomous security operations? The answer depends on execution over the next 18 to 24 months. K7 deployments, federal contract announcements, and revenue acceleration would validate the thesis. Delays, competitive losses, or capital constraints would undermine it. Investors should size positions according to the speculative nature of the opportunity and monitor quarterly results closely.