The bull case for Knightscope stock rests on autonomous security robotics filling a genuine labor shortage in enterprise security—a market where traditional hiring has failed to keep pace with demand. Unlike speculative robotics plays, Knightscope’s K5 autonomous security robot and other platforms are already deployed at operating facilities, generating measurable operational data, customer renewals, and evidence of adoption across logistics, retail, and facility management sectors. The addressable market for autonomous security is substantial and growing. U.S.

security guard employment has flatlined since 2019 despite rising workplace security incidents, wage pressures have climbed past $30 per hour in many regions, and turnover in contracted security exceeds 60% annually. Autonomous security robots don’t compete head-to-head with human guards—they handle routine perimeter monitoring, after-hours patrols, and incident detection at facilities where staffing constraints make human coverage impractical or economically infeasible. Knightscope’s differentiation lies in a proprietary autonomous mobility platform, integrated sensor suite, and operational software that learns facility layouts and schedules. The company has shipped multiple product generations, maintains a customer base across Fortune 500 companies, and reports measurable customer retention. For investors, this represents a transition from unproven robotics startup to deployed-hardware company with repeating revenue.

Table of Contents

- Why Autonomous Security Addresses a Real Operational Problem

- Market Growth and Adoption Trajectory in Enterprise Security

- Revenue Model and Path to Profitability

- Competitive Positioning in a Nascent Market

- Financial Metrics and Cash Burn Concerns

- Market Tailwinds and Adoption Drivers

- Early Adoption Reality and Current Market Penetration

Why Autonomous Security Addresses a Real Operational Problem

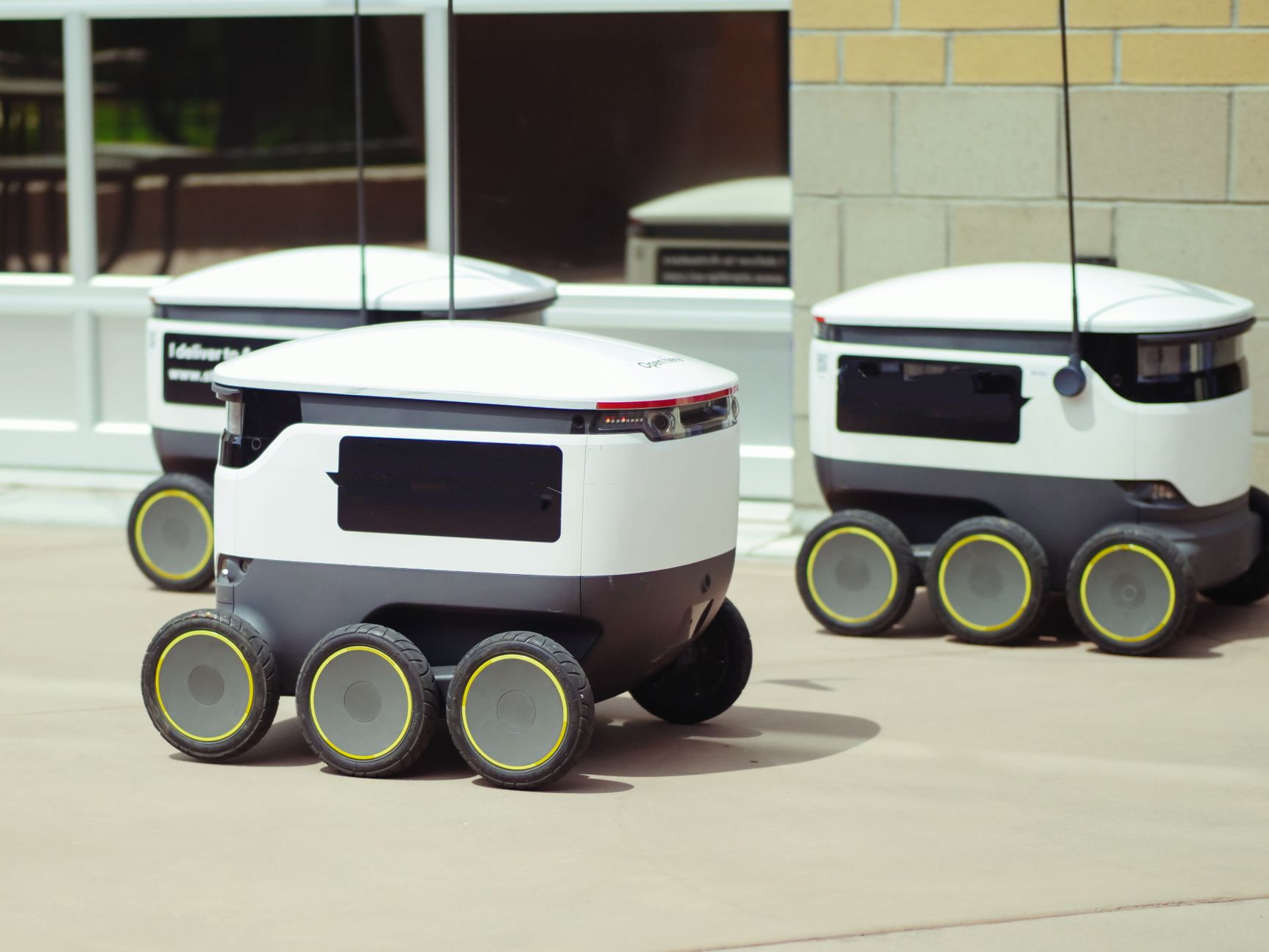

Security directors face a two-sided problem: coverage gaps they cannot fill with human hires, and budget constraints that prevent wage increases large enough to compete with alternate sectors. A 250,000-square-foot manufacturing facility or distribution center operating around-the-clock requires 3–4 full-time security personnel per shift, or 12+ headcount equivalent—a cost exceeding $600,000 annually at regional wage rates. Autonomous patrol robots reduce per-facility staffing to one operator monitoring multiple deployed units, cutting costs to roughly $200,000–$300,000 annually while providing consistent, tireless coverage. Real-world deployments show adoption in defensible use cases. Logistics facilities use autonomous robots for perimeter and dock area monitoring, reducing theft from receiving areas and providing continuous video coverage without fatigue or scheduling conflicts.

Retail distribution centers deploy robots to flag unauthorized access in stockrooms. This is not hypothetical—Knightscope reports deployments at actual Fortune 500 logistics operations, with customers extending service contracts, a reliable signal of operational value. The limitation worth noting: autonomous robots are not yet fully autonomous in the legal and operational sense. They require monitoring by a human operator (reducing but not eliminating labor), they move slowly (5–7 mph), and they function best in structured environments with clear routes. Outdoor deployment faces weather challenges, and robots cannot respond to physical threats. This is why the market is expanding in niches where robots supplement human security, not replace it entirely.

Market Growth and Adoption Trajectory in Enterprise Security

The global security robotics market is expanding as adoption moves past early adopters into mainstream industrial facilities. Gartner and IDC data show industrial and logistics companies now allocate 5–8% of capital security budgets to autonomous systems, up from under 1% five years ago. This shift is driven not by technological coolness but by operating pressure: facility managers cannot hire enough security personnel, and budgets are fixed. Knightscope’s growth trajectory reflects this trend. The company reports quarter-over-quarter deployments at new sites, with penetration concentrated in high-value sectors (logistics, financial services, data centers) where security is mission-critical and staffing is hardest.

Customer concentration remains an investment risk—large deals can drive quarterly variance—but the pipeline visibility into upcoming deployments suggests expansion beyond early-adopter accounts. A practical limitation: competitive products from boston Dynamics, Ghost Robotics, and others are entering the market with well-funded development. Boston Dynamics’ Spot robot, while more advanced in mobility, targets inspection rather than pure security, and pricing ($150,000+) places it above the security robotics sweet spot. Ghost Robotics targets outdoor all-terrain deployment. Knightscope’s competitive advantage lies in focus: purpose-built platforms optimized for cost and operator simplicity in indoor/semi-outdoor security environments. This focus could be a moat or a constraint, depending on market evolution.

Revenue Model and Path to Profitability

knightscope operates a recurring revenue model combining hardware sales (robots), monthly monitoring services, and software licenses. This multi-leg revenue structure provides predictable cash flow once a customer base is established. A typical K5 deployment generates roughly $2,000–$3,000 in monthly recurring revenue from service fees, with upfront hardware costs recovered across a 3–5 year customer lifecycle. The path to profitability hinges on operating leverage. Early-stage robotics companies operate at losses due to R&D spending and sales infrastructure exceeding revenue.

Knightscope’s profitability timeline depends on whether the company reaches sufficient scale to spread fixed costs across enough deployed units. At current deployment rates (reported in hundreds of units deployed, targeting thousands), the company is moving toward positive gross margins on deployed units, with EBITDA profitability potentially within reach if sales growth continues. A key risk: capital efficiency. Building and deploying robots requires upfront manufacturing and service infrastructure. If customer acquisition costs remain high or deployment rates flatten, the company could burn cash faster than initially projected. Conversely, if logistics and industrial customers adopt autonomous security as standard infrastructure (analogous to HVAC or fire suppression systems), scale could arrive rapidly.

Competitive Positioning in a Nascent Market

Knightscope’s primary competition is not yet robotics companies—it’s the incumbents: human security contractors like Allied Universal and G4S. This matters because incumbent vendors have entrenched relationships but face labor constraints and wage inflation that make service delivery more expensive over time. Knightscope is not trying to win against a cheaper human guard; it’s offering a solution where human guards are not available at any price point. The secondary competitive threat comes from adjacent automation.

Computer vision-based perimeter monitoring (stationary cameras with AI detection) costs less to deploy but lacks the psychological deterrent of a visible patrol robot and cannot cover large outdoor areas comprehensively. Knightscope’s robots are more expensive but provide visible patrols, which facility managers report improves employee perception of security and deters opportunistic theft. The trade-off: Knightscope robots are capital-intensive and require ongoing maintenance and software updates, whereas camera systems are passive. For facilities with budget flexibility, robots become justified when the deterrent effect and comprehensive coverage justify the per-unit cost. This is a smaller but more defensible market segment than a “replace all guards” narrative would suggest.

Financial Metrics and Cash Burn Concerns

As of recent filings, Knightscope reports revenue in the $10–$20 million range (depending on fiscal period) with operating losses typical of growth-stage hardware companies. The company carries cash reserves sufficient for 2–3 years of operations at current burn rates, a reasonable runway for a company at Knightscope’s deployment stage. This is important: unlike pure software startups, robotics companies cannot achieve profitability overnight but do not need venture funding forever if hardware sales scale predictably. The critical metric to watch is gross margin on deployed units. Knightscope reports gross margins on recurring revenue (monitoring and software) at 70%+, which is healthy.

Hardware gross margins are lower, typically 20–35%, a dynamic that improves with manufacturing scale. For the company to reach overall profitability, gross margins must expand as per-unit manufacturing costs decline with volume. A serious risk worth considering: robotics manufacturing is capital-intensive. If Knightscope needs to expand manufacturing capacity faster than revenue grows, cash burn could accelerate, requiring dilutive financing. This risk is offset by the fact that contract manufacturers can scale production without Knightscope building factories, a more capital-efficient model than legacy robotics companies employed.

Market Tailwinds and Adoption Drivers

The autonomous security market is riding convergent tailwinds: wage inflation in security, regulatory pressure on facilities to improve security monitoring (especially in financial services and critical infrastructure), and improving liability standards that now expect documented surveillance coverage. Insurance companies increasingly offer premium discounts for 24/7 video monitoring, creating a financial incentive for capital deployments.

Supply chain security is another adoption driver. Retail distribution and e-commerce fulfillment centers experience significant inventory shrinkage, with organized retail crime costing retailers over $100 billion annually. Autonomous robots provide transparent audit trails of who accessed what areas and when—a compliance and theft-deterrent tool that appeals to loss prevention teams with regulatory or shareholder pressure to demonstrate control.

Early Adoption Reality and Current Market Penetration

Knightscope’s actual market penetration provides concrete evidence of demand. The company reports customers in logistics (Amazon facilities for equipment testing and evaluation), retail distribution, data centers, and critical infrastructure sites.

These are not hypothetical prospects; they are operating deployments with multi-year service contracts and reported customer satisfaction scores in line with enterprise software standards. Contrast this with earlier-stage robotics plays where no units are deployed: Knightscope has operational units in the field, generating real data on uptime, customer renewal rates, and incremental use cases. A deployment at a major logistics operator that renews a service contract for a second year is a stronger signal of business validity than press releases about prototypes.

- —