Agility Robotics, the humanoid robot maker behind the Digit bipedal robot, announced on June 24, 2026, that it will go public through a merger with Churchill Capital Corp XI, a special-purpose acquisition company (SPAC). The deal values Agility at $2.5 billion and is expected to generate over $620 million in gross proceeds, with approximately $200 million coming from new and existing institutional investors. Upon completion, Agility will trade under the ticker symbol AGLT on a North American stock exchange, marking a significant moment for the robotics industry. The move positions Agility as the first US-listed pure-play humanoid robotics company to reach public markets.

This distinction matters because it signals investor confidence in a sector that has attracted billions in venture capital but has rarely taken the traditional IPO path. Agility’s willingness to pursue this route reflects not just technological progress but the company’s confidence in near-term commercial viability, backed by customers already running Digit robots in production environments. The company’s timing reflects genuine market traction, not speculative positioning. Digit has accumulated over 65,000 hours of real-world operational experience across nine customer sites, a metric that separates Agility from many competitors still working through prototype phases.

Table of Contents

- Why SPAC Instead of Traditional IPO? Understanding Agility’s Path to Public Markets

- Digit’s Specifications and Commercial Limitations

- Real-World Deployment with Established Companies

- The Investor Backing and What It Signals

- Becoming the First US-Listed Pure-Play Humanoid Robotics Company

- Production Capacity and Manufacturing Scale

- Market Timing and the Robotics Inflection Point

Why SPAC Instead of Traditional IPO? Understanding Agility’s Path to Public Markets

A SPAC merger differs from a traditional IPO in structure and speed, but serves similar ends: raising capital and achieving public listing status. For Agility, this approach sidesteps the lengthy underwriting process of a conventional IPO while still accessing public capital markets. The SPAC route has become common in robotics and emerging tech because it allows companies to make forward-looking business projections without triggering the strict regulatory limitations placed on traditional IPO roadshows.

The deal’s structure—with $200 million from new and existing institutional investors alongside Churchill Capital Corp XI’s capital—reflects a hybrid funding model. Some investors are deepening existing positions; others are entering at the public-company valuation threshold. This mix suggests confidence across both established and new backers, though it also means existing venture investors are effectively taking partial exits while remaining exposed to public market volatility. The $2.5 billion valuation offers a concrete reference point: the company goes public neither undervalued by strategic buyers nor inflated by unfounded speculation.

Digit’s Specifications and Commercial Limitations

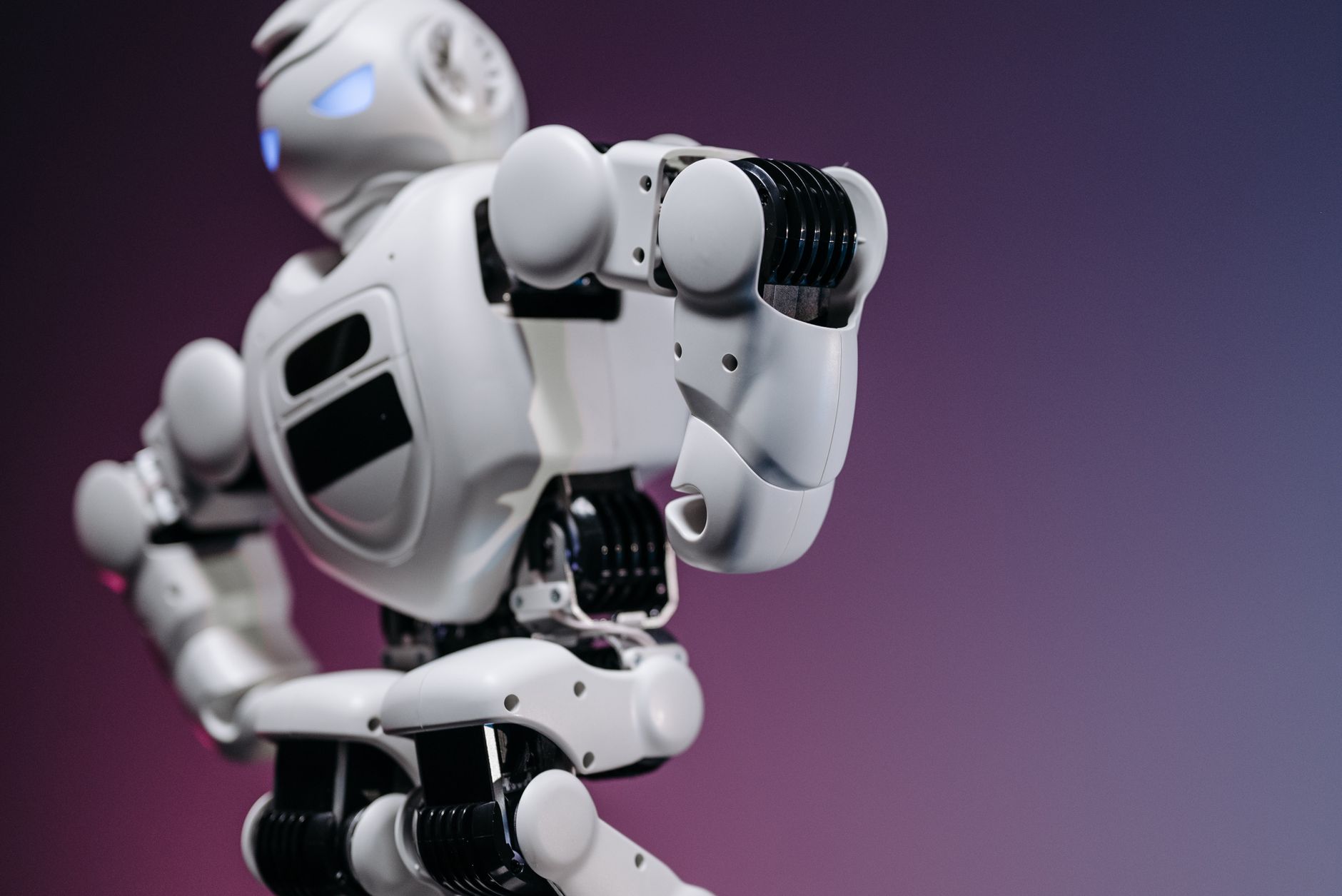

Digit is a bipedal humanoid robot designed for warehouse and logistics environments rather than general-purpose humanoid applications. The robot stands about five feet tall and is designed to move items between storage locations and packing stations, mimicking human movement patterns in confined spaces where traditional wheeled robots struggle. This narrow specialization is both strength and constraint: Digit can be optimized for specific tasks, but it cannot easily pivot to radically different applications without significant redesign. The 65,000 hours of operational experience Agility has accumulated provides a reality check on reliability and performance.

This figure—accumulated across nine different customer sites—suggests Digit handles actual warehouse complexity rather than controlled demonstrations. However, 65,000 hours distributed across multiple customers and years of deployment is substantially different from one robot running 24/7. A single robot at full utilization might accumulate that many hours in roughly seven years. This distinction matters when evaluating reliability claims: distributed operational hours tell you the robots function in real settings, but they do not guarantee the uptime profile needed for continuous production.

Real-World Deployment with Established Companies

Agility’s customer roster anchors the SPAC announcement in tangible commercial reality. Schaeffler, a major automotive supplier; GXO, a leading logistics company; Toyota Motor Manufacturing Canada; and Mercado Libre, Latin America’s largest e-commerce platform, are using Digit robots in live operations. These are not pilot programs or proof-of-concepts—they are customers running robots in existing production workflows. GXO’s engagement is particularly notable: the company signed what Agility describes as the industry’s first commercial humanoid Robot-as-a-Service (RaaS) contract. This contractual model matters because it shifts risk from the customer to Agility.

Rather than Mercado Libre or another customer purchasing robots outright and bearing full maintenance responsibility, GXO pays per unit of work performed. If Digit breaks down frequently, Agility absorbs the cost—a structure that creates strong incentive alignment but also exposes the company to operational risk if units fail at higher rates than the RaaS model assumes. Toyota Motor Manufacturing Canada’s participation adds automotive-sector credibility. In February 2026, Agility signed a production agreement with Toyota, lending manufacturing expertise and scale to the deployment. This partnership suggests Toyota sees near-term volume potential, though the precise terms—how many units, what timeline—remain undisclosed.

The Investor Backing and What It Signals

Agility’s investor base includes Amazon, Nvidia, SoftBank Vision Fund 2, and DCVC—a consortium of companies and funds with different investment theses. Amazon’s participation reflects the company’s interest in warehouse automation and last-mile logistics. Nvidia’s backing connects to the computational power humanoid robots require for perception and control. SoftBank Vision Fund 2’s involvement suggests a longer-term venture capital perspective, while DCVC brings climate and sustainability-focused investment criteria to the table.

This investor diversity creates both stability and potential conflict. Amazon and Nvidia are strategic investors with interest in Agility’s success, but they also pursue competing robotics initiatives internally. Amazon’s Digit deployment could accelerate if Agility falters—or conversely, Amazon might reduce orders if internal robotics programs mature. Nvidia benefits from demand for GPUs powering Digit’s systems regardless of whether Agility succeeds as a public company. The presence of multiple large tech companies in Agility’s cap table reduces extinction risk but complicates questions about independence: does Agility set product roadmap based on customer feedback and market demand, or does Nvidia’s majority in high-performance hardware needs influence product direction?.

Becoming the First US-Listed Pure-Play Humanoid Robotics Company

Agility’s distinction as the first US-listed pure-play humanoid robotics company is meaningful precisely because most robotics companies go public as diversified manufacturers or automation conglomerates. Boston Dynamics, widely regarded as the robotics field’s most advanced humanoid platform, remains private under Hyundai ownership. Sanctuary AI and Figure AI are pursuing funding but have not yet gone public. Agility reaching public markets first creates an optics advantage—the company can claim first-mover status in a category—but also exposes it to higher expectations and scrutiny.

Being the first public company in a category creates benchmarking problems. Investors will compare Agility’s performance—deployment rate, uptime, customer acquisition—against expectations for humanoid robotics, not against robot vacuum or industrial arm manufacturers with established track records. If Digit achieves 95 percent uptime but investors expect 99 percent based on aspirational industry narratives, the stock could suffer despite strong real-world performance. The public market does not always reward early movers; sometimes it punishes them for failing to meet speculative expectations set by venture narratives.

Production Capacity and Manufacturing Scale

The Toyota agreement signed in February 2026 signals Agility’s plans to scale manufacturing beyond current levels. Toyota’s involvement in production implies shared factory space or manufacturing partnerships rather than Agility building greenfield plants independently. This arrangement preserves capital for R&D and customer acquisition but creates dependency: if Toyota reduces its manufacturing allocation, Agility’s production capacity becomes the bottleneck.

Digit’s deployment across nine customer sites suggests current production runs in dozens to low hundreds of units per year. Reaching the scale that justifies a $2.5 billion valuation—hundreds or thousands of robots across multiple customer segments—requires manufacturing to grow substantially. The capital from this SPAC deal will fund both that expansion and the working capital needed to support RaaS models where Agility absorbs operational risk rather than customers purchasing assets outright.

Market Timing and the Robotics Inflection Point

The June 2026 announcement arrives at a moment when humanoid robotics transitions from novelty to commercial deployment. The convergence of three trends—large language models providing reasoning capabilities, advances in actuators and batteries supporting bipedal movement, and warehouse labor costs justifying automation investment—creates genuine business opportunity rather than speculative hype. GXO’s RaaS contract and Toyota’s manufacturing agreement confirm this is not venture capital betting on future potential; it is customers paying for robots that work today.

The 65,000 hours of accumulated operation across nine sites represents the practical proof Agility needed to justify public market entry. This is not a company going public with promises of what humanoid robots might do someday. It is a company going public because customers are already integrating Digit into production workflows and paying for the service. That distinction separates Agility’s SPAC deal from many previous automation company IPOs that promised future adoption and underdelivered.