Agility Robotics has achieved a $2.5 billion valuation through a SPAC business combination, a significant milestone that reflects growing investor confidence in the commercial humanoid robotics sector. This transaction represents one of the largest funding rounds in advanced robotics, signaling that the industry is moving beyond early-stage research and into serious commercialization efforts. The valuation places Agility among the most valuable privately-backed robotics companies, alongside competitors in the autonomous systems and industrial automation spaces. The SPAC structure—merging with a special purpose acquisition company rather than pursuing a traditional IPO—has become increasingly common in the robotics and advanced technology sectors over the past several years.

This approach allows companies to access public capital markets while avoiding some of the regulatory complexity of a direct IPO. For Agility, the transaction provides capital for scaling manufacturing, expanding research and development, and bringing products like the Digit humanoid robot closer to mainstream industrial deployment. The $2.5 billion valuation reflects investor bets on humanoid robotics solving real labor shortages in warehouse logistics, manufacturing, and other industries. However, achieving that vision requires overcoming substantial technical, regulatory, and manufacturing challenges that will test whether the company can deliver on the promise implied by its valuation.

Table of Contents

- What Does a $2.5 Billion SPAC Valuation Mean for Robotics?

- SPAC Mergers in the Robotics Sector—Opportunities and Constraints

- The Humanoid Robotics Market and Competitive Landscape

- Manufacturing Scale and Capital Requirements

- Technical Risk and Regulatory Uncertainty

- Supply Chain Dependencies and Manufacturing Risk

- Capital Efficiency and Path to Profitability

- Frequently Asked Questions

What Does a $2.5 Billion SPAC Valuation Mean for Robotics?

A $2.5 billion valuation positions Agility robotics as a major player in the broader automation sector, but valuation alone is not the same as proven commercial viability. The figure reflects market expectations about the company’s future revenue potential, not its current earnings. For context, early-stage software companies are often valued at similar multiples based on growth potential, while established manufacturing companies typically trade at much lower revenue multiples. Robotics companies occupy a middle ground—they have physical products requiring significant capital investment, but they also promise disruptive market opportunities. The SPAC structure enabled this funding without the need for traditional venture capital rounds or an IPO roadshow. Rather than pitching to dozens of institutional investors, Agility negotiated directly with a SPAC sponsor.

This approach accelerates access to public markets and capital but also shifts risk. SPAC investors are betting on management execution rather than a long operational history. If Agility encounters manufacturing delays or technical setbacks, the stock price could suffer significantly—a risk that traditional venture investors would have spread across multiple rounds. The $2.5 billion valuation assumes substantial future growth in the commercial robotics market. If industrial adoption of humanoid robots accelerates—for instance, if major logistics companies like Amazon or DHL deploy thousands of units for unloading trucks—the valuation could prove conservative. Conversely, if robotics adoption stalls due to technical limitations or regulatory barriers, the valuation will likely face downward pressure.

SPAC Mergers in the Robotics Sector—Opportunities and Constraints

SPAC mergers have become a popular financing route for robotics and autonomous systems companies, largely because they provide faster access to capital than traditional venture funding or IPOs. Companies including Intuitive Machines, Axiom Space, and others in adjacent sectors have used SPAC combinations to fund scaling and product development. The advantage is clear: a company can move from private to public within months rather than years, and the capital comes without the dilution of additional venture rounds. However, SPAC mergers carry specific constraints and risks that should not be overlooked. Public market scrutiny arrives immediately—SEC filings, quarterly earnings calls, and stock price volatility create new pressures that private companies avoid.

Agility will face investor expectations for quarterly progress updates and financial transparency. If product launches slip or market adoption moves slower than anticipated, shareholder pressure could force management to adjust strategy or accelerate timelines unrealistically. Additionally, SPAC investors often include both long-term believers and short-term traders seeking near-term gains. This creates volatility in the stock price and can distract management from long-term product development. Some SPAC mergers have struggled when the reality of bringing cutting-edge technology to market proved more difficult than pre-merger projections suggested.

The Humanoid Robotics Market and Competitive Landscape

Agility’s $2.5 billion valuation reflects the intense competition and investor interest in humanoid robotics specifically. Companies like Boston Dynamics, Tesla (with its Optimus program), and others are pursuing similar technologies, though their funding sources and commercialization timelines vary. Boston Dynamics, despite its advanced capabilities, has remained private and moved slowly toward commercial deployment. Tesla is funding Optimus internally but has not yet released units at scale. This variation in approach means Agility’s SPAC path gives it a distinct advantage: immediate access to capital without dependence on a parent company’s quarterly earnings. The humanoid form factor appeals to investors because robots designed with human-compatible morphology could theoretically integrate into existing industrial environments without major infrastructure changes.

A humanoid robot could potentially work in warehouses, factories, and service environments already built for human workers. This broad applicability explains why valuations in the sector have climbed sharply in recent years. However, the competitive advantage is fragile. The companies closest to commercial deployment—Agility included—are not yet proven at scale. None has deployed thousands of units to real customers. The first company to achieve reliable, cost-effective deployment at scale will gain enormous market advantage. Conversely, if a competitor achieves breakthrough efficiency or reliability before Agility, the valuation could face significant pressure.

Manufacturing Scale and Capital Requirements

Bringing the Digit humanoid robot to production scale will require enormous capital investment beyond the initial $2.5 billion valuation. Building manufacturing facilities, developing supply chains, and maintaining quality control for sophisticated robotics are capital-intensive endeavors. Agility will need to spend heavily on factory automation, quality assurance, and technical support infrastructure just to reach meaningful production volumes. Many robotics companies have underestimated these costs, leading to cash shortages and delayed deployments. The $2.5 billion raised through the SPAC will likely be allocated across several priorities: manufacturing capacity, continued R&D, regulatory approvals, and working capital.

For comparison, traditional automotive manufacturers spend 5-7% of revenue on R&D, while early-stage robotics companies typically spend 15-25% as they work toward product-market fit. Agility will need to balance aggressive scaling with ongoing innovation to keep pace with competitors. Burning through capital without hitting commercial milestones would force the company to return to capital markets before profitability, potentially at a lower valuation if execution falters. The typical path for hardware companies—low initial unit sales followed by exponential growth—requires sustained capital availability and reliable supply chains. Any major disruption, from chip shortages to component availability, could cascade into delayed customer deliveries and eroded investor confidence.

Technical Risk and Regulatory Uncertainty

Humanoid robots operating in real warehouses, factories, and other industrial settings face significant regulatory hurdles that remain incompletely defined. Unlike software or traditional manufacturing equipment, humanoid robots share spaces with human workers and make autonomous decisions. Safety standards for human-robot interaction are still evolving. OSHA, European safety standards, and international regulators have not yet established comprehensive frameworks for mobile humanoid robots in industrial environments. Agility will need to work with regulators to establish safe operating parameters and liability frameworks before large-scale deployment is possible. Technical risk remains substantial despite significant progress in robotics over the past decade.

Humanoid robots excel at controlled tasks in research environments but struggle with the unpredictability of real-world work. Warehouse floors are cluttered, lighting varies, objects have irregular shapes, and the environment is dynamic. Robots that perform reliably in laboratory conditions sometimes disappoint in field deployments. If Digit encounters reliability problems in customer pilots, the negative publicity could undermine Agility’s market position and investor confidence. The $2.5 billion valuation assumes successful navigation of these technical and regulatory obstacles. If Agility discovers fundamental limitations—for instance, if Digit proves incapable of handling the dexterity or endurance required for many warehouse tasks—the company would need to substantially revise product scope or timelines, likely disappointing investors who based their valuations on near-term commercial viability.

Supply Chain Dependencies and Manufacturing Risk

Advanced robotics depend on specialized components—high-performance actuators, sensors, computing hardware, and materials—that are not commodities. Agility’s success depends on securing reliable supplies of these components at scale. Supply chain disruptions, as the global economy experienced during 2021-2023, can cascade through hardware manufacturing programs and delay customer deployments by months or years.

Building redundancy into supply chains adds cost but is essential for risk management. Manufacturing humanoid robots at competitive cost requires either designing for assembly efficiency or automating production. Both approaches take time and capital to perfect. If Agility cannot achieve cost targets—keeping the per-unit cost low enough that customers see reasonable payback periods—adoption will stall regardless of technical capability.

Capital Efficiency and Path to Profitability

The $2.5 billion valuation will attract intense scrutiny around capital efficiency and the path to profitability. Public company investors expect clarity on when Agility will reach breakeven and when it will generate positive free cash flow. For hardware companies, this journey typically spans 5-10 years from significant capital investment to sustained profitability. Tesla took roughly a decade to reach consistent profitability despite enormous capital raises.

Agility will face investor pressure to demonstrate progress on unit economics—the gross margin and operational efficiency of each robot sold. The challenge is that the first hundreds or thousands of units sold will likely be unprofitable as Agility establishes manufacturing processes, resolves design issues, and optimizes supply chains. Only as volume climbs and manufacturing matures should unit economics improve. If this process extends beyond investor expectations, confidence will erode and stock price will follow.

- —

Frequently Asked Questions

Why did Agility Robotics choose a SPAC merger instead of a traditional IPO?

SPAC mergers provide faster access to public capital and avoid some of the extended SEC review process associated with traditional IPOs. The transaction can close in months rather than years, and Agility negotiates directly with one SPAC sponsor rather than pitching to dozens of institutional investors.

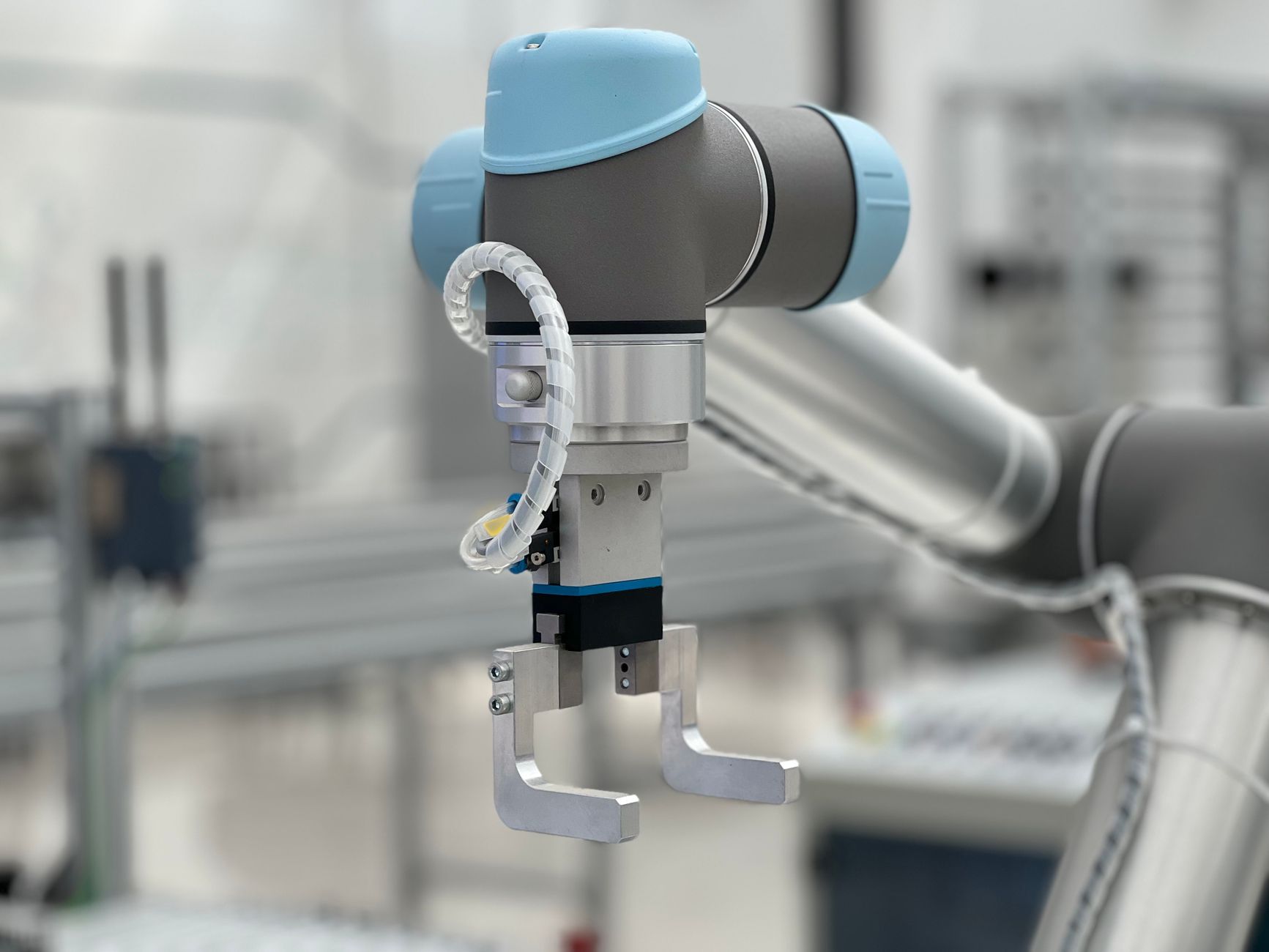

What is the Digit robot, and what will it do?

Digit is Agility’s humanoid robot platform designed for industrial tasks like loading, unloading, and sorting in warehouses and factories. It is designed to work in human environments without major infrastructure changes, but it is not yet deployed at meaningful scale.

How does Agility’s valuation compare to other robotics companies?

At $2.5 billion, Agility ranks among the most valuable private robotics companies globally. For comparison, traditional manufacturing equipment suppliers trade at much lower valuations relative to revenue, while some early-stage software companies achieve higher valuations despite lower revenue.

What are the main risks to Agility’s success?

Technical risks include achieving reliable performance in unpredictable warehouse environments, regulatory risks include safety standards still being developed, manufacturing risks include scaling production efficiently, and market risks include customer adoption rates proving slower than projected.

Will humanoid robots actually replace warehouse workers?

Humanoid robots are positioned as tools to augment or assist human workers in dangerous or repetitive tasks, not necessarily to replace them outright. Labor economics, regulatory frameworks, and technical capability will all influence how widely they are adopted.

When will Digit robots be available for commercial use?

Agility has announced plans for commercial deployment, but specific timelines are not disclosed in the publicly available information. Early pilot customers may receive units before broader market availability.