Teradyne holds a genuine premium valuation amid the accelerating shift toward AI automation, and recent trading activity demonstrates both the market’s confidence and its volatility around this thesis. The stock closed at $369.09 on July 3, 2026, a sharp 13.63% single-day decline that followed a 6.03% jump to $463.21 just four trading days earlier on June 29—a reminder that premium-priced stocks face outsized swings when sentiment shifts. Despite this recent volatility, Teradyne’s year-to-date gain of approximately 140% and its 297.6% return over the past twelve months reflect sustained investor belief in the company’s transformation from a semiconductor test equipment specialist into a diversified player across chip testing, robotics, and factory automation. The valuation premium is substantial and measurable.

Teradyne trades at a forward price-to-sales ratio of 13.43X compared to its semiconductor equipment peer group average of 7.64X—roughly 76% above sector norms. Its forward EV/EBITDA multiple sits near 49X, positioning it above peers like Applied Materials at 40X and Lam Research at 47X, though below none of its direct comparables. That premium sits on a foundation: the physical AI products Teradyne demonstrated at Automate 2026 in June are deployable today, not promises for tomorrow, and the company’s integrated test solutions for data center AI chips address real, immediate infrastructure bottlenecks. The question for investors is whether execution in new market segments will justify a valuation that already prices in substantial growth.

Table of Contents

- How Teradyne’s Valuation Premium Compares to Semiconductor Equipment Peers

- The Robotics and Manufacturing Automation Opportunity

- Physical AI Deployment at Automate 2026

- Test Infrastructure Innovation for AI and Data Center Scaling

- Valuation Risk and Recent Market Volatility

- Analyst Expectations and the Price Target Spectrum

- Execution Risk in Expanding Beyond Core Semiconductor Testing

How Teradyne’s Valuation Premium Compares to Semiconductor Equipment Peers

Teradyne’s 13.43X forward price-to-sales ratio looks aggressive when placed beside the semiconductor equipment industry average of 7.64X. The gap widens further when examining absolute multiples: a 49X forward EV/EBITDA places Teradyne ahead of most equipment makers, though the spread is narrower than headlines sometimes suggest. Advanced Micro Devices’ test equipment partner ASML trades at 36X forward EV/EBITDA, while Advantest—the Japanese competitor most directly comparable in chip test—sits at 32X. Applied Materials and Lam Research occupy the 40X–47X range, making Teradyne’s 49X the high end of the peer set without being an absolute outlier.

This premium reflects the market’s judgment that Teradyne’s diversification into robotics and factory automation offers growth rates faster than traditional semiconductor equipment cycles. But therein lies the risk: the premium assumes Teradyne executes new product lines at semiconductor equipment margins while defending its existing test business against competition from Advantest and KLA-Tencor. If the robotics division grows slower than priced in, or if capital expenditure cycles in semiconductors weaken, the multiple compression could be severe. Historical precedent matters here—semiconductor equipment companies rarely trade above 50X EV/EBITDA unless their growth justifies it, and reversions to historical means can erase years of gains in months.

The Robotics and Manufacturing Automation Opportunity

Teradyne is pivoting from a pure-play semiconductor test vendor into a competitor across three distinct markets: semiconductor testing, manufacturing robotics, and logistics automation. The June 8, 2026, announcement of an integrated test cell solution developed with Tokyo Electron—pairing Teradyne’s UltraFLEXplus platform with Tokyo Electron’s Prexa SDP—signals the company’s strategy to embed itself deeper into the AI and data center chip manufacturing pipeline. These are devices destined for graphics processing and training infrastructure, market segments with both high volume and premium pricing. The broader robotics and logistics push represents a departure from Teradyne’s historical wheelhouse.

The company is targeting complex manual tasks in factories and warehouses—material handling, palletizing, inspection—where manual labor costs are rising and AI-driven automation can deliver measurable ROI. This market is substantially larger than semiconductor testing by addressable revenue, but it is also far more competitive, with established players like ABB, Fanuc, and Kuka already entrenched. Teradyne enters with capital, technology, and Teradyne Robotics as a distinct brand. The limitation here is clear: success requires execution across two fundamentally different sales channels—the long, relationship-driven cycles of semiconductor capital equipment and the faster, project-based cycles of factory automation. Managing both simultaneously is operationally complex and historically prone to distraction-driven underperformance at diversified hardware companies.

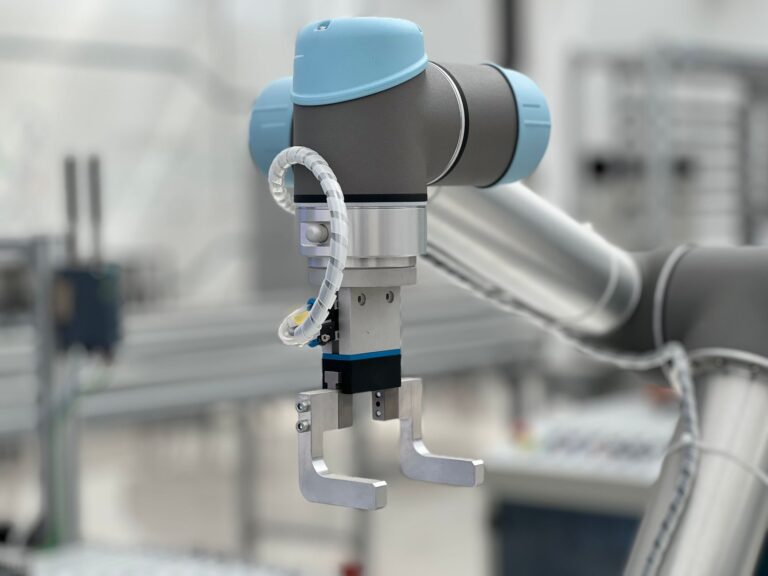

Physical AI Deployment at Automate 2026

At the Automate 2026 conference held June 22–25 in Chicago, Teradyne Robotics showcased products described internally as “real and deployable,” a critical distinction in a market saturated with research prototypes and vaporware. The centerpiece was the MiR1200 Pallet Jack, a mobile manipulation platform capable of autonomous pallet handling in unstructured warehouse and factory environments. This is not a theoretical product or a research arm concept; units are in the field working with customers today. The concrete advantage is meaningful: a working system in June 2026 beats a promised system in 2027, especially in a market where every quarter of delay means competitors gain customer relationships and operational data.

The MiR1200 addresses a specific, expensive problem: autonomous palletization and pallet movement in facilities where manual labor is unavailable or cost-prohibitive. A single pallet jack operator costs roughly $35,000–$45,000 annually in wages and benefits in the US, plus benefits and recruitment churn; deploying even a few MiR1200 units can pay for itself within 18–36 months depending on utilization rates and facility design. But this business model depends on Teradyne’s ability to manage customer implementations, handle software updates, and maintain fleet uptime across dispersed locations. Semiconductor testing is a capital sale with implementation support; robotics requires ongoing service and optimization relationships. The operational demands are substantially different, and overstretch is a real risk.

Test Infrastructure Innovation for AI and Data Center Scaling

The June 8 announcement of the integrated test cell solution for AI and data center device screening is not ceremonial; it responds to a genuine bottleneck in semiconductor manufacturing. As demand for AI training chips accelerates, foundries face constraints in testing capacity—screening millions of devices for defects before shipment requires time, specialized equipment, and skilled operators. The partnership between Teradyne and Tokyo Electron combines two essential functions: Teradyne’s UltraFLEXplus handles electrical testing and characterization across thousands of pins and complex test vectors, while Tokyo Electron’s Prexa SDP handles precision wafer handling and positioning. Together, they cut test time per device and reduce human labor in the test cell.

This is a classical play in semiconductor equipment: integrate horizontally, raise customer switching costs, and price based on the cost savings the customer achieves. If a customer can test 20% more chips per hour with the integrated solution, the ROI math favors investment in the combined system over cobbling together independent tools. But integration also raises Teradyne’s risk. If Tokyo Electron fails to deliver reliably, or if customer requirements diverge from what the partnership assumed, Teradyne becomes partly responsible for outcomes beyond its direct control. Semiconductor fabs are precision operations with razor-thin margins on yield and throughput; any integration misstep can cascade into customer frustration and lost repeat business.

Valuation Risk and Recent Market Volatility

The 13.63% single-day drop on July 3, 2026—two days before this article’s publication date—illustrates the vulnerability of premium-multiple stocks to negative sentiment. Teradyne’s stock had risen to $463.21 on June 29, but reversed sharply within days. In a rising interest rate environment or during any macroeconomic correction, high-multiple growth stocks face disproportionate pressure; the calculus that justified a 49X EV/EBITDA at 2% risk-free rates becomes less supportive at 4% or 5%. Investors who bought near $463 now face double-digit paper losses in just weeks, a reality that underscores the premium’s fragility.

The valuation risk is compounded by concentration of thesis among three major analysts. Cantor Fitzgerald, Bank of America, and Susquehanna have all raised price targets to $550 in late June 2026, but Street consensus remains $399—a divergence of 38% between the bulls and the average. This gap suggests that consensus opinion remains skeptical of the premium despite recent upgrades. If the three major bulls were to downgrade or go silent, consensus would likely reset sharply lower. Investors should approach premium-multiple stocks with extreme caution during periods of multiple compression; the upside from a $399 consensus to a $550 target assumes continued expansion of valuation multiples, a dynamic that historically reverses without warning.

Analyst Expectations and the Price Target Spectrum

As of late June 2026, Teradyne faced a wide range of Street estimates. Cantor Fitzgerald raised its target to $550 from $400, Bank of America upgraded to $525 from $365 with a Buy rating, and Susquehanna maintained a $550 target raised from $415 with a Positive rating. These three represent the bullish consensus, each betting that Teradyne’s diversification into robotics and AI automation will drive earnings growth sufficient to justify current or higher valuations.

Conversely, the broader Street consensus of $399 implies skepticism—a belief that either the diversification will underperform or that current margins in robotics are lower than in semiconductor testing, requiring years of volume growth to offset. The divergence is substantial enough that it merits investor scrutiny. When three major houses raise targets above a consensus line, it signals either that (1) consensus has updated too slowly and the market will soon reprice upward, or (2) the bullish houses are overestimating execution and will eventually lower targets, dragging consensus down. Historical precedent slightly favors the latter in hardware diversification cases; companies expanding into adjacent markets often surprise on the downside relative to initial optimistic projections.

Execution Risk in Expanding Beyond Core Semiconductor Testing

Teradyne’s core semiconductor testing business is mature, capital-efficient, and margin-rich—but it faces long-term headwinds as more testing migrates embedded to chip design or to foundry facilities. Pivoting into robotics and manufacturing automation is strategically sound, but operationally hazardous. The company must recruit and retain world-class robotics engineers, build partnerships with industrial automation integrators, develop service and support infrastructure in geographies where Teradyne has no history, and defend profitability against entrenched competitors with decades of customer relationships.

The risk is not that robotics will fail, but that it will grow more slowly than the valuation assumes or that it will canibalize margins from the core test business. Teradyne’s year-to-date gain of 140% and its 297.6% return over the past twelve months are extraordinary, but they rest on execution assumptions that have not yet been stress-tested through a full economic cycle. The company must deliver on products announced at Automate 2026 and make the Tokyo Electron partnership genuinely productive for customers. If either stumbles, the premium multiple will find no support.

- —